NEWS

Wednesday 5 June 2019

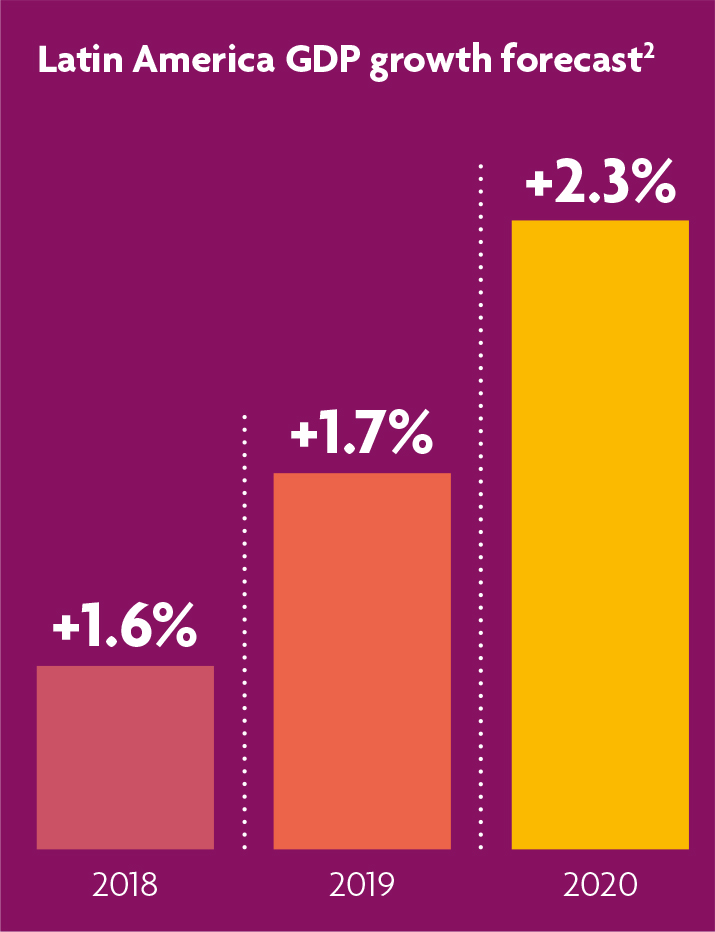

Latin America is undoubtedly one of the world's fastest growing emerging markets. With a combined Gross Domestic Product (GDP) of US$5.97 trillion (2017), compared to just US$3.94 trillion 10 years earlier1, the region has grown hugely and only looks set to continue on that path. Banking giant BBVA recently forecast that Latin America’s GDP will grow 1.7% in 2019 and a further 2.3% in 2020, after already increasing 1.6% in 2018.2

There is no question that both industrial growth and significant market reforms over the past 30 years have helped the region’s development, and have helped it to develop into a market-driven economic bloc. And while substantial economic and political differences still exist between Latin American countries, the region has continued to grow at a consistent rate – although we should note it has been slower than the likes of the United States, Europe and China.

“Latin American-based corporations have been drawn to captives and the benefits they can provide, like cost containment, underwriting profit, stronger governance, better claims analytics and risk management.”

And as the economic bloc has evolved, so has captive insurance sector in the region. Just as in more mature economies, Latin American-based corporations have been drawn to captives and the benefits they can provide, like cost containment, underwriting profit, stronger governance, better claims analytics and risk management.

Yet, while setting up a captive is now fairly commonplace in Europe and North America, the captive sector in Latin America isn’t quite as established. MultiLatinas (Latin American corporations) have not yet fully adopted captive structures to cover either property and casualty (P&C) or employee benefits (EB). So, why has the market lagged behind the rest of the world and what is the potential for captives in the region?

Latin America “the new frontier” for captives

While it has been estimated that there were around US$90 billion written in annual premiums through captives in 2017, less than US$3 billion of those came from Latin American based companies. This might not be surprising given that there were only approximately 115 captives owned by Latin American companies at the time, despite the fact that the region is home to more than 230 companies with revenues over US$1.25 billion. These numbers make it abundantly clear that there’s a huge opportunity for these large multinationals to take advantage of the captive structure and grow the market in the region.3

The Latin American captive market was one of the key topics at this year’s World Captive Forum and generated a lot of interest and conversation. At the event, Tim Faries, Managing Partner at law firm Appleby, said the region represented “a significant opportunity, which has been a long time developing… There are hundreds of companies in the region whose risk financing and management could be improved through a captive. We think Latin America is the new frontier for the captive concept.”3

“There are hundreds of companies in the region whose risk financing and management could be improved through a captive. We think Latin America is the new frontier for the captive concept.”

And so begs the question – why is the region lagging behind the rest of the world in the captive space?

Although Latin American risk managers have known about captive insurance for years, it’s possible the concept is not as widely understood as it is in other markets and this has resulted in their use being less common than in other emerging economic regions. This is the case, perhaps surprisingly, in Brazil, the region’s largest economy, as well as in Argentina and Peru – all are also considered to be behind the curve in the captive space.

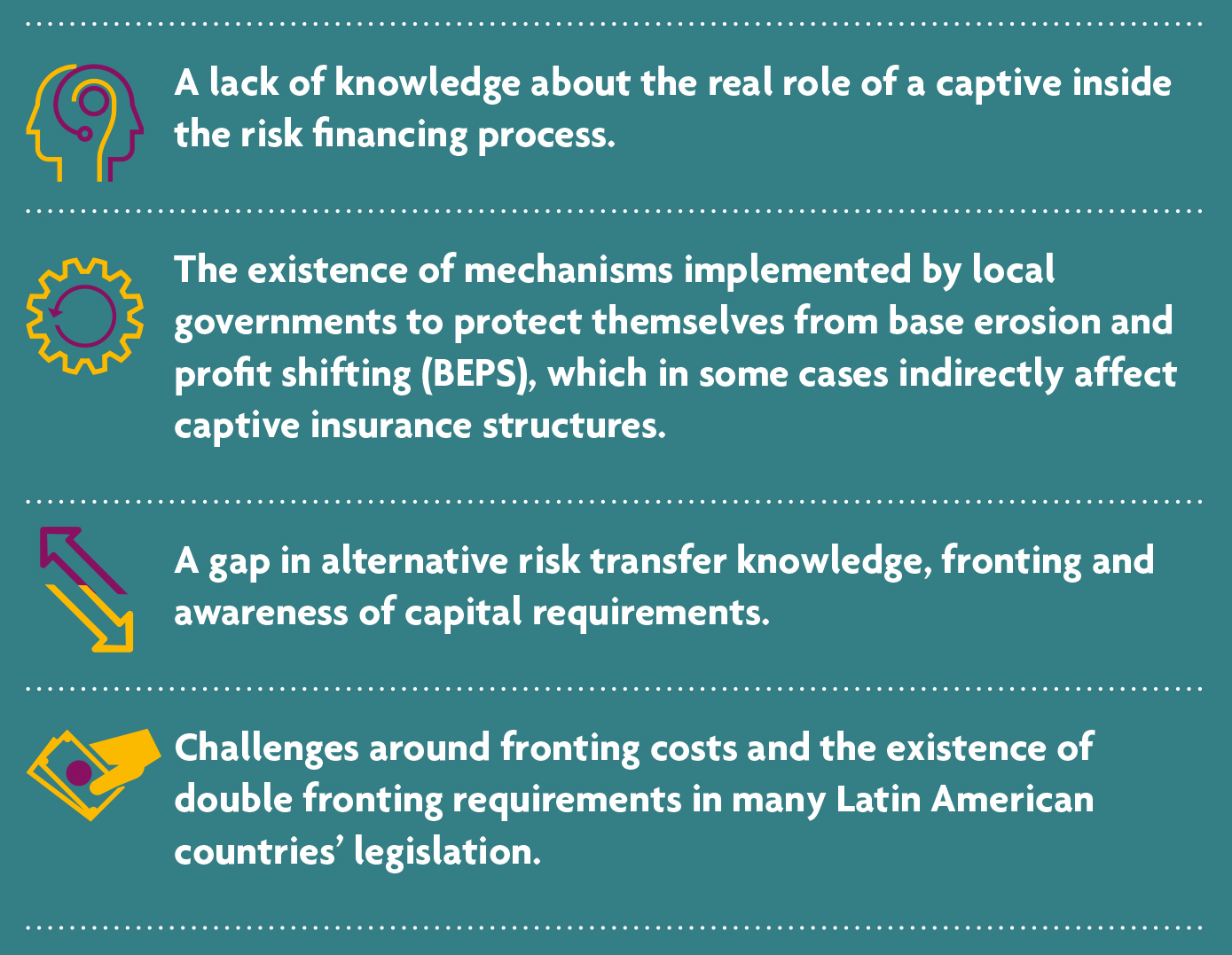

And while it’s hard to pinpoint exactly why the take up of captives has been slower in these countries, there are a few reasons why Latin American companies may not yet have adopted it as a risk management structure.

Having said all of that, some Latin American countries are more active in this space: Mexico and Colombia in particular are further ahead in their implementation of captives than others in the region.

A ‘captivating’ opportunity for Latin America

Having been in place now for over 50 years, the benefits of captive structures are well recognised and there is definite growth in the number of businesses using a global captive. While, as discussed, this is slower in some regions, the positive impact on risk management, underwriting profit and cost control are starting to appeal to multinationals globally.

Having been in place now for over 50 years, the benefits of captive structures are well recognised and there is definite growth in the number of businesses using a global captive. While, as discussed, this is slower in some regions, the positive impact on risk management, underwriting profit and cost control are starting to appeal to multinationals globally.

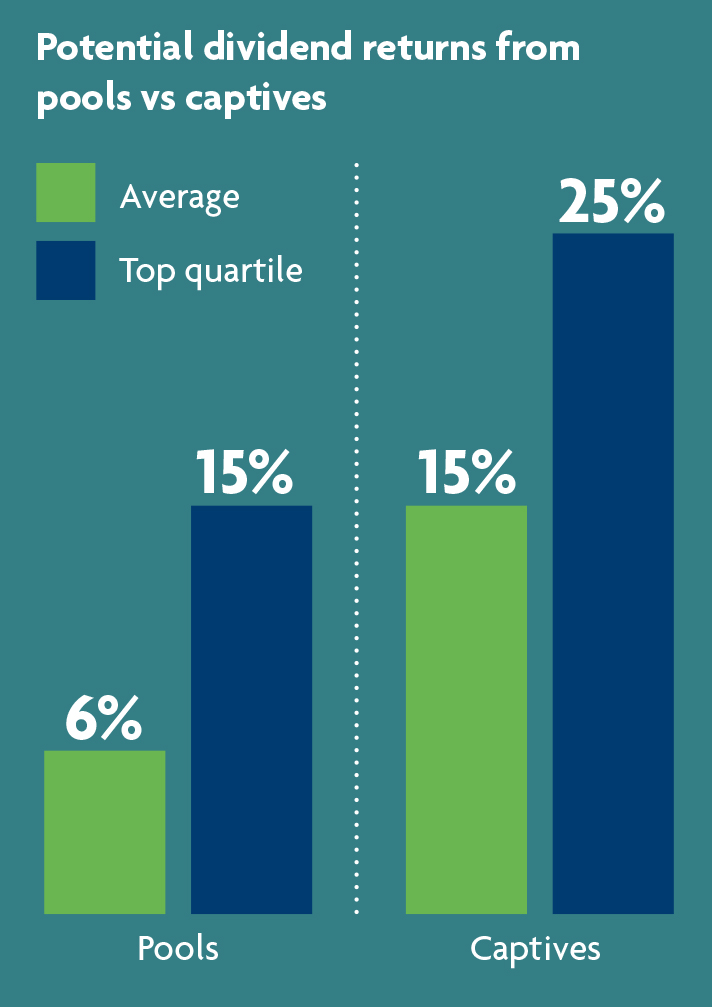

Willis Towers Watson discovered one of the reasons captive structures can be so appealing, particularly for employee benefits. It reports average dividend returns for multinational pools of 6%, with top quartile results producing dividends of over 14%, compared to employee benefit captives which had median surpluses of 15% while the top quartile produced 25% or more.4

Employee benefits are mostly short tail, low impact risks – where claims are usually made during the term of the policy or shortly after the policy has expired5 – meaning pricing is well understood and allows a captive to diversify its insured risks. With adequate protection in place – depending on the size of the captive reinsurer, the exposures in terms of high sums insured or concentration risks – captives are well suited to write all lines of employee benefits and can add significant value for a Latin American multinational employer.

Not only are captives a good vehicle for risk control, they could play a role in tackling the rising cost of medical treatment, too. Running at a minimum of three times the general rate of inflation, covering medical costs is an expensive

business for multinationals globally and is a real problem in Latin America. The region saw an 11.4% rise in medical costs in 2018 alone.6

With increasing claims and rampant medical trend costing multinationals more than ever, a captive structure could play a significant role in helping tackle these growing costs by centralising underwriting processes and allowing much greater control for HR and Risk teams.

“Not only are captives a good opportunity for risk control, but they could play a role in tackling the rising cost of medical treatment, too.”

What challenges do MultiLatinas face when moving towards a captive structure?

While the benefits seem too great to ignore, there are of course some challenges to implementing a captive in Latin America. One of the biggest of which is the differing regulation across countries in the region. While this is changing, more needs to be done and regulatory barriers need to be lowered before the captive model can become more commonplace.

There are positive signs, though. Recent legislation in Argentina means premium can now be ceded out of the country for the first time in years. Following a set schedule, the percentage reinsured will go up in incremental

portions over the next few years up to a max of 75%. Other countries in the region have also amended their capital requirements, but this would only affect employee benefits captives domiciled in the region.

When it comes to employee benefits, decentralisation of the benefits process might also be a barrier Latin American companies will need to overcome. For example, a lot of traditional cross-border Latin American companies started as local family businesses that typically grew through acquisitions. This means their HR and risk management functions, including compensation and benefits, have not always been managed centrally – which can be an issue for effective management of a global EB programme.

Mauricio Suarez, Americas Business Development Manager at MAXIS GBN, believes that this lack of centralisation could mean that current P&C captive owners are the most likely to move towards an EB captive.

“The region is behind the curve on centralising its benefits, so over such a short window the best prospects to have an employee benefits captive would be those that already have a P&C captive. But for that group of MultiLatinas, securing authorisation from the regulatory bodies in their captive’s status can be a drawn-out procedure which could last up to 12 months – as we are seeing first-hand. However, it is worth persevering.”

“A lot of traditional cross-border Latin American companies started as local family businesses that typically grew through acquisitions, meaning their HR functions, including compensation and benefits, have not always been managed centrally – which can be an issue for effective management of a global EB programme.”

Conclusion

Conclusion

While interest in the captive concept has grown in recent years, Latin American companies looking to move towards an employee benefits captive will need to overcome both regulatory challenges and a potential lack of EB central management to be able to maximise the benefits of a captive structure. But there is reason for optimism. As the market becomes more aware of the benefits of captives and centralised benefits programmes, and traditional broker houses drive collaboration between their P&C and EB divisions, MultiLatinas may be able to start reaping the rewards of captive structures over the coming years.

To find out more about MAXIS GBN’s coverage in this region, please contact Mauricio Suarez or download our Latin America brochure.

1 World Bank, https://data.worldbank.org/indicator/NY.GDP.MKTP.CD?locations=ZJ (source April 2019)

2 BBVA Research https://www.bbvaresearch.com/en/category/regions-en/latin-america/ (source April 2019)

3 Ned Holmes, Captive Insurance Times http://www.captiveinsurancetimes.com/captiveinsurancenews/article.php?article_id=6232 (source April 2019)

4 Willis Towers Watson, https://www.willis.com/documents/publications/services/captives/Multinational-Pooling-Captive-Ben-Survey.pdf (source April 2019)

5 Lloyds, https://www.lloyds.com/help-and-glossary/glossary-and-acronyms?Letter=S (source April 2019)

6 Willis Towers Watson, https://www.willistowerswatson.com/-/media/WTW/PDF/Insights/2017/12/2018-global-medical-trends-pulse-survey-report-wtw.pdf (source April 2019)

This document has been prepared by MAXIS GBN and is for informational purposes only – it does not constitute advice. MAXIS GBN has made every effort to ensure that the information contained in this document has been obtained from reliable sources, but cannot guarantee accuracy or completeness. The information contained in this document may be subject to change at any time without notice. Any reliance you place on this information is therefore strictly at your own risk. This document is strictly private and confidential, and should not be copied, distributed or reproduced in whole or in part, or passed to any third party.

The MAXIS Global Benefits Network (“Network”) is a network of locally licensed MAXIS member insurance companies (“Members”) founded by AXA France Vie, Paris, France (AXA) and Metropolitan Life Insurance Company, New York, NY (MLIC). MAXIS GBN, registered with ORIAS under number 16000513, and with its registered office at 313, Terrasses de l’Arche – 92 727 Nanterre Cedex, France, is an insurance and reinsurance intermediary that promotes the Network. MAXIS GBN is jointly owned by affiliates of AXA and MLIC and does not issue policies or provide insurance; such activities are carried out by the Members. MAXIS GBN operates in the UK through UK establishment with its registered address at 1st Floor, The Monument Building, 11 Monument Street, London EC3R 8AF, Establishment Number BR018216 and in other European countries on a services basis. MAXIS GBN operates in the U.S. through MetLife Insurance Brokerage, Inc., with its address at 200 Park Avenue, NY, NY, 10166, a NY licensed insurance broker. MLIC is the only Member licensed to transact insurance business in NY. The other Members are not licensed or authorised to do business in NY and the policies and contracts they issue have not been approved by the NY Superintendent of Financial Services, are not protected by the NY state guaranty fund, and are not subject to all of the laws of NY. MAR00427/0519