Looking at the new indicator of employee engagement and productivity

NEWS

Monday 3 July 2017

London, UK

When you survey an average group of workers about what keeps them awake at night, you’ll find that financial concerns regularly top the list of issues that cause people to feel stressed. And as we know, the impact of this stress on employees at work can be severe, with distraction and lost productivity just two of the side effects of money worries.

The fact that the global population is predicted to live longer is only adding to those financial concerns. Workers approaching retirement, in particular, face difficult decisions about whether they will outlive their retirement funds and what they can do about it – right now. For younger employees, the questions are around how much later they will need to work to build up an adequately comfortable pension, meet the inevitably rising costs of a longer old age and save for this while the cost of living is high.

Evidence from MetLife’s Employee Benefit Trends Study in markets such as Australia and the United Kingdom (UK) suggests that less than 30% of employees are very confident in their ability to make financial decisions about their retirement plans. Those who are stressed at work by financial concerns are more likely to report health issues, miss work and be distracted by their financial situation while at work.

The World Health Organisation has called stress the “health epidemic of the 21st Century” and it’s estimated that it costs US businesses up to $300 billion a year through lost productivity and absence. Personal finance is not only the leading cause of stress but also requires time to sort things out when they go wrong. Just as more employers see the value of providing employee health and stress management programmes, so a growing number of employers are investigating the possibility of setting out financial wellness programmes for staff, programmes that aim to prevent the problem arising in the first place. And it’s a problem that could really benefit from prevention rather than cure. Financial worries are very real concerns for a large proportion of the global workforce. MetLife’s EBTS in the UK asked employees: “How concerned are you about the following financial issues at this time?”? The respondents ranked them as follows:

- job security

- having financial security for their family in the event of their premature death

- financial security for their family if a principal income earner isn’t able to work due to disability or serious illness

- having too much credit card debt

- affordability of their children’s education.

PwC’s Financial Wellness Survey further makes the point that younger generations in countries such as the US and UK may need specific help with their ability to pay back student loans. Its research found that 81% of Millennials and Gen X employees with significant student loan debts were stressed about their finances compared to 45% who did not have this extra burden. As stated in MetLife’s EBTS conducted across several markets, an effective financial wellness programme can help employers:

- bolster productivity because employees aren’t distracted by financial worries

- drive more predictable workforce flow throughout the organisation

- increase employee engagement and retention

- create more affordable retirement options for all employees and enable career advancement opportunities for younger employees.

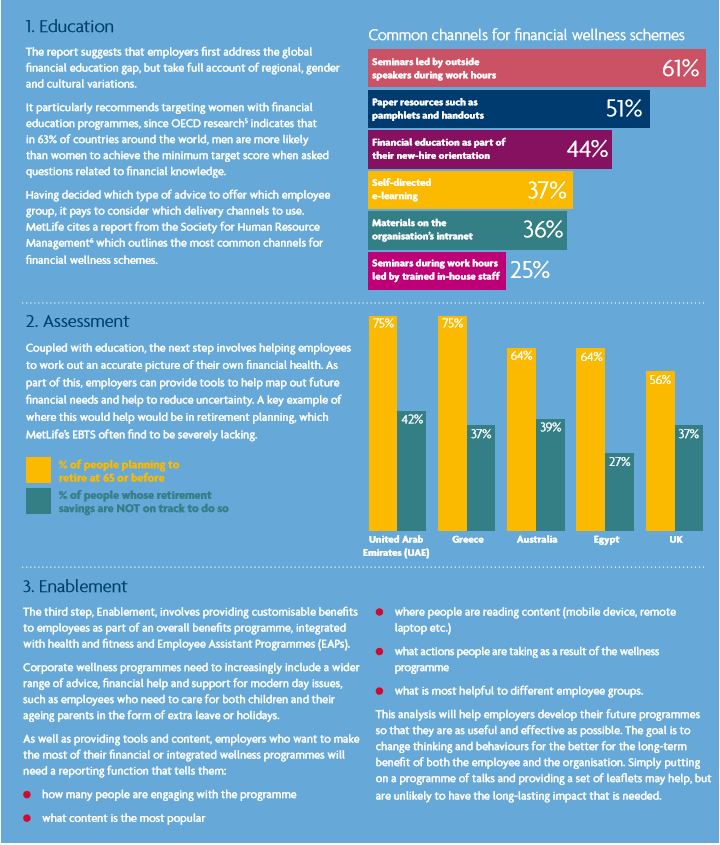

So, where do organisations that do not have a financial wellness programme in place already, begin? In its report entitled The Emerging Practice of Financial Wellness4 , MetLife outlines a useful three step approach based on Education, Assessment and Enablement.

A note of caution however …

While this type of financial wellness support will no doubt be both welcome and beneficial, employers must always remember that their staff members’ privacy needs to be safeguarded at all times. New data protection legislation arriving in the shape of the General Data Protection Regulations (GDPR) in Europe in May 2018 makes this an even greater consideration.

A careful balance must also be struck between being a helpful source of advice and help and being seen as interfering too much in employees’ private financial matters.

There are already some commentators who criticise health and wellness programmes for being discriminatory and personally intrusive: could the natural conclusion of a poorly managed financial wellness programme be that individuals are ‘marked down’ for being poor managers of their own personal finances? Could their careers suffer because of it?

Overall and on balance, however, the reasons for having financial wellness programmes in place are wholly positive, from attracting people to want to work for you to addressing the stress epidemic and the productivity gap.

For all of these reasons, we can expect more organisations to adopt financial wellness programmes as part of their overall employee engagement strategies in the years ahead. The key to their success will be ensuring that programmes are targeted, flexible, appropriate, measurable and well-communicated. Improved levels of employee engagement and productivity will be the outputs to calculate and monitor.

-----------

Unless otherwise noted, data and statistics are sourced from the MetLife’s Employee Benefit Trends Study developed in Australia (2017), Egypt (2015), Greece (2017), UAE (2014), and the UK (2017).

1. PwC’s 2017 Employee Financial Wellness Survey, 2017 https://www.pwc.com/us/en/private-company-services/publications/financial-well-being-retirement-survey.html

2. GOBankingRates.com – should this not be a source?, August 2016 https://www.gobankingrates.com/personal-finance/financial-stress-state/

3. Mercer, Zen and the Art of Employee Financial Wellness https://www.uk.mercer.com/what-we-do/wealth-and-investments/employee-financial-wellness.html

4. MetLife, The Emerging Practice of Financial Wellness, 2017 benefittrends.metlife.com

5. OECD research, 2013 http://www.oecd.org/daf/fin/financial-education/OECD_INFE_women_FinEd2013.pdf

6. Society for Human Resource Management Society for Human Resource Management, “Financial Wellness in the Workplace,” May 2014